Políticas de salud

← vista completaPublicado el 25 de octubre de 2017 | http://doi.org/10.5867/medwave.2017.08.7054

Efectividad de los impuestos a bebidas azucaradas para reducir niveles de obesidad: resumen de evidencia para políticas

Effectiveness of sugar-sweetened beverages taxes to reduce obesity: evidence brief for policy

Resumen

La alta prevalencia de obesidad en Chile en conjunto con el creciente consumo de bebidas azucaradas en el país, han permitido plantear las medidas fiscales por medio de los impuestos a alimentos específicos, como una alternativa complementaria de abordaje a este problema. Desde 2014 se encuentra en vigencia en Chile un alza adicional de 5% del impuesto a las bebidas analcohólicas azucaradas, magnitud eventualmente insuficiente para producir impacto en los niveles de obesidad.

La evidencia de efectividad de las medidas fiscales a bebidas azucaradas en términos de modificación de precio, en general muestra un alto traspaso del impuesto al consumidor, lo que varía según condiciones locales. El análisis de la literatura, reveló una sensibilidad de la demanda a los cambios de precios de las bebidas azucaradas por medio de elasticidades negativas cercanas a -1 para distintos grupos observados, junto con la disminución en el consumo de estos productos. Por su parte, los efectos en peso corporal tras la aplicación de estos impuestos fueron analizados por diversos estudios de simulación. Éstos reportaron disminución de prevalencia de obesidad entre 0,99% y 2,4%. En relación a la aceptabilidad de una medida fiscal de esta naturaleza se presentaron cifras variables de apoyo entre 36 y 60% en población general. Respecto a los eventuales efectos negativos en empleos, un estudio internacional incluso demostró un alza en las cifras de empleo en dos estados tras la aplicación de un impuesto a bebidas azucaradas.

La búsqueda bibliográfica demostró que existe evidencia para fundamentar la implementación de una medida fiscal a bebidas azucaradas en Chile. Sin embargo, faltan estudios de simulación locales que permitan explorar los eventuales efectos e implicancias de un nuevo impuesto de este tipo en el país. Las medidas fiscales a alimentos parecen ser alternativas viables y efectivas para abordar el problema de la obesidad en Chile, pero deben considerarse como parte de una estrategia integral, con el fin de lograr un impacto final en la disminución de prevalencia de obesidad en el país.

Resumen ejecutivo

Introducción: Chile presenta altas cifras de obesidad (25,1%) [1],[2], con una tendencia al alza y mayor presencia en sectores de menor nivel educacional. Además, se evidencia en la población chilena un alto y creciente consumo de bebidas azucaradas, contribuyendo al aumento de prevalencia de obesidad de la población [3]. Las medidas fiscales, por medio de impuestos a alimentos específicos, podrían jugar un rol complementario a otras medidas tradicionalmente implementadas, desincentivando el consumo de alimentos asociados al exceso de peso. Dentro de las últimas medidas fiscales implementadas en Chile, destaca un aumento de 13 a 18% del impuesto adicional a las bebidas analcohólicas (IABA), vigente desde el año 2014. Si bien se reconoce un avance en esta materia, la evidencia internacional sugiere que un aumento de esta magnitud sería insuficiente para generar impacto en la prevalencia de obesidad. En este contexto, surge la pregunta sobre cuál es la evidencia que sustenta las políticas fiscales de este tipo en términos de su efectividad para modificar los precios, la demanda y sus efectos en salud.

Evidencia de efectividad de las políticas fiscales sobre bebidas azucaradas:

- Efectos del impuesto en el precio: un estudio en población mexicana evidenció 100% de traspaso del impuesto a los precios hacia el consumidor. Asimismo, tres estudios realizados en Berkeley mostraron porcentajes menores de traspaso (entre 21,7 y 47%), aunque bajo condiciones locales que pudiesen explicar dichas cifras [4],[5],[6],[7].

- Efectos del impuesto en la demanda de bebidas azucaradas: se evidencia una sensibilidad a los precios, disminuyendo el consumo ante las alzas de estos. Cuatro estudios en Latinoamérica, incluyendo Chile, demostraron elasticidades negativas cercanas a - 1, ligeramente superiores a otros hallazgos en revisiones sistemáticas y metanálisis de la literatura internacional [8],[9],[10],[11],[12],[13],[14],[15].

- Efectos del impuesto en el consumo: destaca un estudio realizado en población mexicana, que dio cuenta del cambio en el consumo de bebidas azucaradas posterior a la aplicación del impuesto de un peso mexicano por litro. Se observó una disminución promedio de 6%, con una reducción máxima de 12% para el último mes observado. Las cifras se acentuaron en hogares con bajo nivel socioeconómico [16]. Un estudio realizado en Berkeley demostró también un efecto posterior al impuesto, con una disminución de 21% en el consumo [17].

- Efectos del impuesto en el peso corporal: se encontraron 18 estudios de simulación y dos metanálisis que dan cuenta de este aspecto. Los principales resultados revelan la mayor efectividad en un impuesto volumétrico (centavos por litro) versus impuesto ad valorem para generar impactos en el peso de la población. Diversos estudios que proyectaron un impuesto de un centavo de dólar americano por litro de bebida azucarada, reportaron resultados de disminución de prevalencia de obesidad en 0,99 y 2,4%; cifras variables según año de medición y grupo etario involucrado [2],[18],[19],[20],[21],[22],[23],[24],[25],[26],[27],[28],[29],[30],[31],[32],[33],[34].

Aceptabilidad y consideraciones de implementación:

- Con respecto a las opiniones de los actores involucrados, nueve estudios reportaron evidencia en este aspecto. En población general, se informan niveles variados de apoyo (entre 36 y 60%) a una medida fiscal a bebidas azucaradas. La evaluación de la opinión de actores involucrados, principalmente personajes políticos, en proceso de toma de decisión de políticas sanitarias es distinta. Dicha evaluación presenta cifras de apoyo ligeramente menores, aduciendo a factores económicos y a potestad del Estado para interferir en libertades personales [35],[36],[37],[38],[39],[40],[41],[42],[43]. Una investigación cualitativa realizada en Chile tuvo por fin el explorar el contexto político ante el alza de impuestos de 5% a bebidas azucaradas implementada en 2014. Se detectó como un importante argumento en contra, la inexistencia de estudios de efectividad locales que respaldaran la medida. Además, se identificó la necesidad de abordar globalmente el problema de la obesidad [44].

- En cuanto al proceso político, destacan dos análisis en torno a las consideraciones en el diseño de un impuesto a bebidas azucaradas y su aplicación. Se señalan factores clave en el éxito de la medida, como el tipo de impuesto a aplicar, tipo de bebida a gravar y su tasa correspondiente. Además, se realiza un análisis exhaustivo de la situación local por medio de conocimiento acabado de la prevalencia de obesidad, consumo de bebidas azucaradas e impuestos vigentes [45],[46].

- Dos estudios se refieren a eventuales efectos negativos, asociadas a empleo y sustitución. Una simulación realizada por Powell con una tasa de 20% en bebidas azucaradas en los estados de Illinois y California, evidenció un aumento en las cifras de empleo en ambos estados de 0,06 y 0,03%, respectivamente [47].

- Considerando la potencial sustitución de las bebidas azucaradas por otros productos de alta densidad calórica, un estudio exploró el cambio a través del consumo de otros alimentos ante una medida fiscal de este tipo, reportando una disminución global en la compra diaria de 24,3 kilocalorías por persona, sin encontrarse evidencia de reemplazo con otros alimentos azucarados [48].

Conclusiones: la búsqueda bibliográfica arroja evidencia que demuestra que la demanda de bebidas azucaradas es elástica a las modificaciones de precio y que los impuestos se traspasan a los precios de los consumidores. Destaca la experiencia mexicana de un impuesto de un peso mexicano por litro, que reporta disminución global del consumo, lo que se acentúa en población de nivel socioeconómico bajo. Los estudios que evaluaron impacto en peso corporal correspondieron en su gran mayoría a estudios de modelamiento, demostrando que alzas de precio del producto gravado mayores a un 10% tendrían un impacto positivo en salud. Al respecto, es importante mencionar que la reciente reforma tributaria en Chile generó un aumento de 5% en el precio en bebidas azucaradas, el cual podría resultar insuficiente para generar cambios de conducta que lleven a producir efectos en salud.

Las consideraciones de diseño e implementación de una medida fiscal son múltiples. Chile presenta condiciones que lo posicionan como un país que podría verse beneficiado ante la implementación de una medida de esta naturaleza. Ante la aplicación eventual de una política a bebidas azucaradas en Chile, deberán hacerse públicas las consideraciones locales y la naturaleza de le medida fiscal con el fin de informar correctamente a la población general, tomadores de decisión e industria. Resulta fundamental también generar más estudios locales que permitan explorar los efectos e implicancias de un nuevo impuesto a bebidas azucaradas, de manera de complementar la experiencia internacional con evidencia nacional. Las medidas fiscales a alimentos para enfrentar los problemas de obesidad de la población parecen ser alternativas viables y efectivas, pero deben considerarse como parte de una estrategia y no una solución por sí misma. Además, deben estar insertas dentro de un programa nacional que contemple el abordaje global del problema.

Introducción

Los altos niveles de obesidad representan un problema prioritario de salud pública en nuestro país, dada su importante asociación a enfermedades crónicas no transmisibles, su consiguiente morbimortalidad, la carga de enfermedad asociada a ellas y el gasto económico en su tratamiento.

Las cifras de prevalencia de obesidad en Chile no son alentadoras. Presentan una tendencia al alza, con una prevalencia actual de 25,1% en población general según la última Encuesta Nacional de Salud [1]. A menor nivel educacional, esta cifra aumenta a 35,5%. Mediciones sucesivas durante los últimos años revelan un aumento sostenido de esta cifra en todos los grupos etarios. La Encuesta Nacional de Salud del año 2003 evidenció una prevalencia de obesidad general de 23,2%, versus 25,1% para el año 2009 [49].

Las bebidas azucaradas son productos de amplia disponibilidad y consumo en nuestra población, asociados a mayor probabilidad de obesidad [50], diabetes mellitus 2 [51],[52], hipertensión arterial [53] e insuficiencia renal crónica [54]. Chile presenta cifras de consumo que ameritan un análisis desde la perspectiva de la salud pública, de modo de complementar las estrategias vigentes que abordan el problema de obesidad en el país. Actualmente, Chile lidera el ranking mundial de aporte calórico por bebestibles, por medio de un venta diaria promedio de 188 kilocalorías per cápita de bebidas azucaradas, dejando atrás a países con altos índices de consumo de estos productos como México (158 kilocalorías diarias) y Estados Unidos (157 kilocalorías diarias) [3]. No sólo la cifra en sí misma es preocupante, sino la importante tendencia al alza que ha presentado durante los últimos 30 años.

Dada la multicausalidad del problema de la obesidad, el enfrentamiento de esta temática debe provenir de múltiples frentes. En Chile, se realizan actividades de educación y promoción de la salud, asociado a intervenciones clínicas en el nivel primario de atención de salud, principalmente a través del Programa Vida Sana.

Con respecto a intervenciones a través de medidas de regulación y fiscalización, se realizan permanentes actualizaciones al Reglamento Sanitario de Alimentos. Últimamente se han impulsado modificaciones a la legislación vigente, especialmente en la Ley Sobre Composición Nutricional de los Alimentos y su Publicidad y el incremento al Impuesto Adicional a Bebidas Analcohólicas. Este impuesto representa 0,5% del total de la recaudación nacional por medio de impuestos y 0,1% aproximado del producto interno bruto nacional [55].

Actualmente, los impuestos específicos a alimentos representan un tema de amplía discusión, encontrándose en fase de implementación en varios países del mundo como políticas fiscales para enfrentar los índices de obesidad. La racionalidad de estas medidas apunta a generar incentivos para modificar ciertos patrones de consumo, además de corregir externalidades negativas asociadas a su ingesta. Se perfilan como una alternativa complementaria para enfrentar la obesidad de la población en países de alta prevalencia. Dentro del grupo de impuestos a alimentos, destaca como un grupo particular el impuesto a bebidas azucaradas, respaldado por numerosos estudios que lo sugieren como una política fiscal promisoria al ser aplicada en conjunto con otras estrategias.

Actualmente en Chile, y tras la reforma tributaria del año 2014, el impuesto específico a las bebidas analcohólicas azucaradas aumentó de 13 a 18%, disminuyéndose en 3% el impuesto a las bebidas de menor contenido de azúcar, perfilándose como la única política fiscal vigente en nuestro país para enfrentar la prevalencia de obesidad. Si bien se reconoce el avance en esta temática, la experiencia internacional sugiere que la magnitud de la medida sería insuficiente para generar impactos en salud [34],[56].

Este resumen tiene por fin dar cuenta de la experiencia internacional y evidencia disponible en los últimos años sobre impuestos aplicables a bebidas azucaradas como política pública para prevenir la obesidad, con el objeto de informar procesos de decisión en la materia. Se describen las principales alternativas de impuestos implementados por medio de modelamiento o experiencias locales. Además se incorporan consideraciones sobre los procesos políticos e implementación de una medida de este tipo, con el fin de entregar un marco de información ante nuevos procesos de toma de decisión con respecto al uso de políticas fiscales para reducir el consumo de bebidas azucaradas en Chile. Las consideraciones metodológicas de la búsqueda de evidencia, así como tablas de resumen de cada uno de los estudios, se detallan en los Anexos.

Evidencia de efectividad de las políticas fiscales sobre las bebidas azucaradas

Los efectos de las intervenciones fiscales pueden dividirse en efectos sobre los precios, sobre la demanda, sobre el consumo y sobre resultados en salud. A continuación se presenta una síntesis de evidencia para cada uno de estos efectos:

1. Efecto del impuesto en los precios:

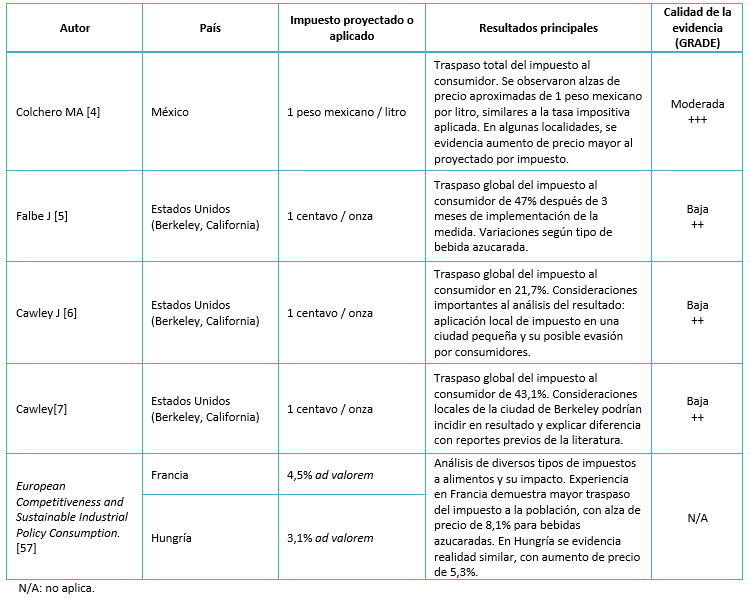

1.1 Un estudio pseudoexperimental aplicado en México evidencia un traspaso total del impuesto al consumidor, con un alza de los precios similar a la proyectada por el impuesto. Incluso se observó en zonas urbanas una sobrecarga en los precios en bebidas carbonatadas mayor a la dada por el impuesto vigente [4].

1.2 Tres estudios implementados en la ciudad de Berkeley, California [5],[6],[7], Estados Unidos, estudiaron el traspaso de un impuesto de un centavo por onza, vigente desde noviembre de 2014. Estos concluyeron un traspaso de 21,7%, 43,1% y 47%, menores a los esperados. Como factor limitante importante de la experiencia en Berkeley, se plantea la aplicación de un impuesto a nivel local, en una ciudad de superficie pequeña que facilita la evasión del impuesto tras la compra del producto en una ciudad vecina, con una demanda elástica de los consumidores dada la disposición geográfica [6],[7].

1.3 Otras experiencias demostraron un traspaso del precio al consumidor mayor al esperado por el impuesto aplicado. Al segundo año de su aplicación, un impuesto de 4,5% a bebidas azucaradas en Francia generó un aumento de precio de 8,1% del producto. La misma experiencia se repitió en Hungría, donde un impuesto 3,1% se tradujo en aumento de precio de 5,3% de bebidas azucaradas [57]. (Tabla 1).

Tamaño completo

Tamaño completo 2. Efecto del impuesto en la demanda:

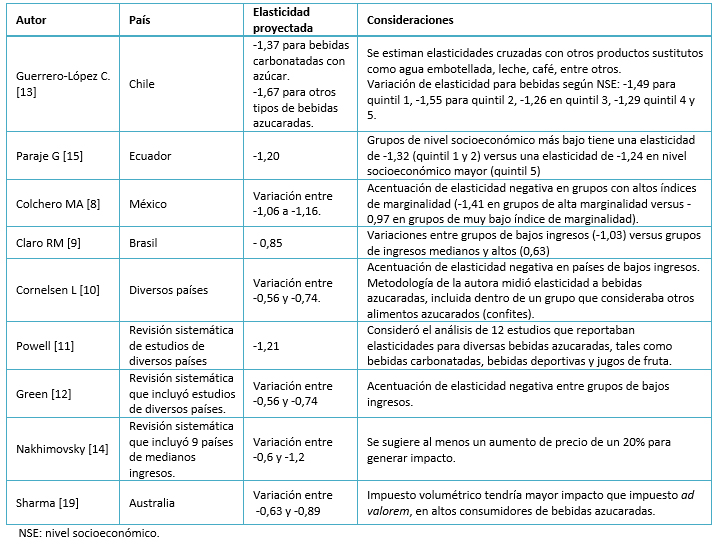

2.1 La literatura demuestra que los consumidores son sensibles en su demanda de bebidas ante cambios en los precios. En el caso de las bebidas azucaradas, la evidencia consistentemente demuestra que la demanda es elástica.

2.2 La búsqueda bibliográfica arrojó cuatro estudios en Latinoamérica, que evidenciaron una elasticidad de -1,37 para Chile [13]; - 1,17 y -1,33 según nivel socioeconómico para Ecuador [15]; -1,06 a -1,16 en México [8] y de -0,85 en Brasil [9] para las bebidas azucaradas. En tanto, revisiones sistemáticas y meta-análisis refuerzan estos hallazgos, por medio de elasticidades negativas entre -0,56 y 0,74 [10], -1,21 [11], -0,6 a -1,2 en países de medianos ingresos [14] y -0,74 a -0,56 para Green y colaboradores [12], según grupo socioeconómico. (Tabla 2)

Tamaño completo

Tamaño completo 3. Efecto del impuesto en el consumo:

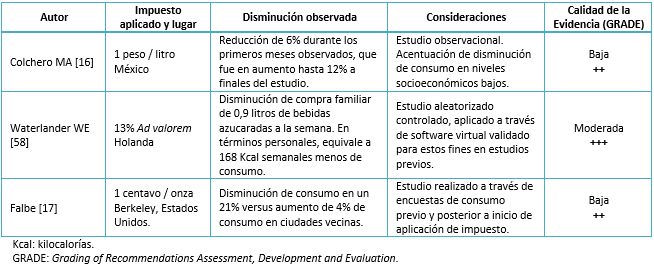

3.1 Un estudio observacional aplicado en población mexicana, da cuenta del consumo de bebidas azucaradas y el cambio posterior a la aplicación del impuesto de un peso mexicano por litro (alza aproximada de 10% del valor previo al impuesto) en enero de 2014. Se observa una disminución promedio en el consumo de bebidas azucaradas en 6%, presentándose una aceleración en su disminución para los últimos meses observados, con una reducción de 12% para el mes de diciembre de 2014. La disminución en el consumo fue mayor en hogares de bajo nivel socioeconómico. Además, se observó un aumento de 4% del consumo de bebidas sin nuevos impuestos, principalmente a través del aumento de la ingesta de agua embotellada [16].

3.2 A través de un estudio aleatorizado controlado, Waterlander y colaboradores analizan los potenciales efectos de un alza de 13% de impuesto a bebidas azucaradas en los países bajos, por medio de un software de supermercado virtual validado en estudios anteriores. Los resultados arrojaron una disminución de compra familiar de 0,9 litros semanales, lo cual llevado a niveles individuales se refleja en una disminución de 400 mililitros semanales por persona, con una equivalencia en calorías de 168 kilocalorías menos de consumo por individuo a la semana. No se encontraron cambios significativos en la compra de otros productos del supermercado [58].

3.3 Datos recientes que surgen asociados a la experiencia de Berkeley, demostraron una disminución del consumo de bebidas azucaradas en 21%, posterior a la implementación del impuesto, en comparación a ciudades vecinas (sin impuesto) donde se registró un aumento de 4% del consumo de dichos productos [17]. Se observó además un aumento del consumo de agua en 63%, en comparación con otras ciudades vecinas donde se reportó un aumento de consumo de 21%. (Tabla 3)

Tamaño completo

Tamaño completo 4. Efectos de un impuesto en el peso corporal:

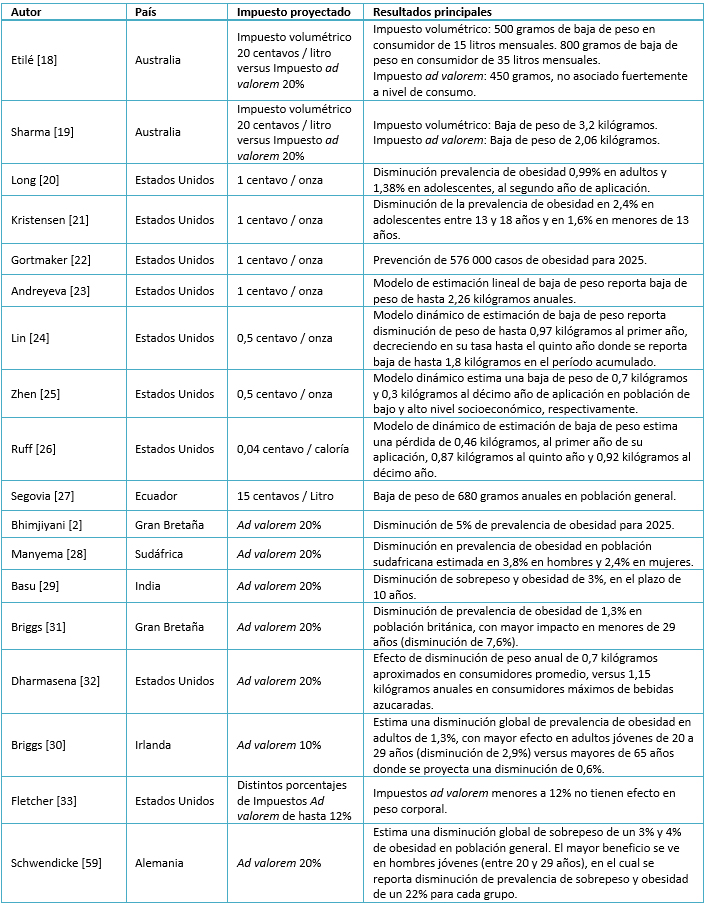

4.1 Se encontraron 18 estudios de modelamiento [2],[18],[20],[21],[22],[23],[24],[25],[26],[27],[28],[29],[30],[31],[32],[33],[59] y tres revisiones sistemáticas [34],[60],[61] que dan cuenta de este aspecto. Destaca la amplia variedad de escenarios, métodos y fuentes de información que deben considerarse al interpretar los resultados.

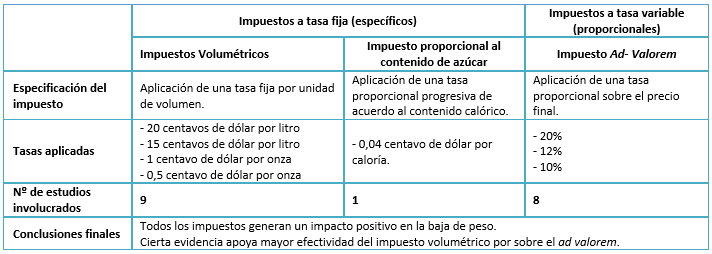

4.2 Se identifican en los estudios principalmente tres tipos de impuestos: impuestos volumétricos a bebidas azucaradas (un centavo de dólar por onza, por ejemplo), impuestos ad valorem, que considera gravar en un porcentaje determinado el precio final del producto (por ejemplo, 20% de impuesto ad valorem) y finalmente impuestos proporcionales al contenido de azúcar (por ejemplo un centavo de dólar por gramo de azúcar). Los estudios de modelamiento y sus principales resultados se encuentran detallados en la Tabla 4. De los resultados, destaca una mayor efectividad relativa de un impuesto volumétrico versus el impuesto ad valorem para medir efectos en baja de peso, sobretodo en poblaciones de alto consumo. De la búsqueda, sólo un estudio estimó efectos de un impuesto proporcional al contenido de azúcar (0,04 centavo de dólar por caloría) [26]. (Tablas 4 y 5)

Tamaño completo

Tamaño completo  Tamaño completo

Tamaño completo 4.3 En relación a los impuestos específicos volumétricos, los estudios que lo proponen en su mayoría lo valorizan como un centavo de dólar por onza (una onza líquida equivale a 29,5 centímetros cúbicos) de bebida azucarada. Destaca una asociación positiva del impuesto con disminución en la prevalencia de obesidad, proyectándose disminuciones entre 0,99% y 2,4% [18],[19],[20],[21], variables según año de medición y grupo etario involucrado. A este respecto se estima una prevención de 576 000 casos de obesidad para 2025, en población norteamericana [22].

4.4 La estimación de baja de peso varió entre los distintos estudios, según la metodología aplicada. Si bien en todos los estudios de modelamiento incluidos en este reporte se documentó algún grado de impacto positivo en peso, la magnitud del efecto es dependiente de la aproximación metodológica adoptada [24],[25]. Maniadakis y colaboradores, a través de una revisión sistemática, destacan la escasa evidencia en peso corporal existente de las medidas fiscales a alimentos [61].

4.5 Un estudio de simulación realizado en Ecuador, proyecta un impuesto volumétrico de 15 centavos por litro de bebida azucarada en población ecuatoriana, el cual indicó una baja de peso de 680 gramos anuales en población general [27].

4.6 Seis estudios de modelamiento y dos revisiones sistemáticas concluyen un potencial efecto en baja de peso corporal ante un impuesto ad valorem de 20% [2],[28],[29],[31],[32],[34],[59],[60]. Tasas menores a 12% no tendrían un impacto positivo en el peso corporal. Como excepción a lo anterior, Briggs evidencia que un impuesto ad valorem de 10% en población Irlandesa, determinaría una baja de peso asociada a su implementación [30]. En el otro extremo, solo una revisión sistemática plantea que, si bien el consumo de un alimento gravado puede disminuir, esta disminución tiene una traducción discreta en la baja de peso [61].

Aceptabilidad y consideraciones de implementación:

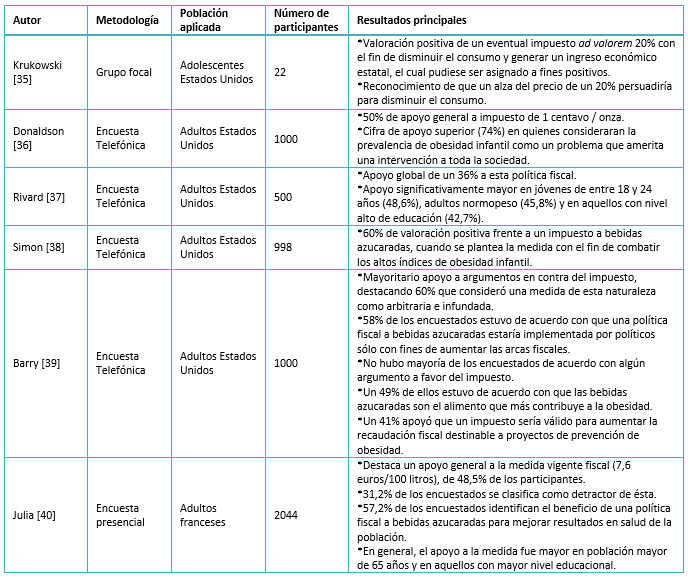

• Aceptabilidad de la medida fiscal: con respecto a las opiniones de consumidores generales ante una política fiscal para bebidas azucaradas, la búsqueda reportó diversos estudios de opinión, la mayoría representativos de población estadounidense. Del total de estudios, cinco son aplicados en población general cuyos resultados son resumidos en la Tabla 6 [35],[36],[37],[38],[39],[40]. Se reportan distintos niveles de aceptación con un porcentaje de apoyo que varía entre 36% y 60%. Principalmente, las variaciones se dan entre los distintos niveles de educación (mayor apoyo en nivel alto de educación) y calificación de índice de masa corporal (mayor apoyo en encuestados normopeso).

Tamaño completo

Tamaño completo Niederdeppe y colaboradores estudian el impacto mediático de una propuesta fiscal a través de la evaluación de la prensa escrita estadounidense. Se contabilizó mayor porcentaje de noticias con mensajes que apoyan esta medida (83%), bajo argumentos de beneficios en salud y de recaudación fiscal. Dentro de los mensajes en contra de esta política destacaron las implicancias negativas en la economía y una intrusión gubernamental inadecuada [43].

Se realizó una entrevista a 18 stakeholders clave con experiencia en medidas fiscales, con el fin de valorar el impacto y efectividad de mensajes a favor y en contra de impuestos a bebidas azucaradas. Los mensajes a favor de la medida de mayor identificación por los entrevistados, se asociaron a las externalidades negativas en salud del consumo excesivo de bebidas azucaradas (obesidad y diabetes) y los beneficios sociales de la inversión de la recaudación del impuesto. Los mensajes en contra de la medida con mayor identificación se relacionaron a un potencial impacto económico negativo de la política, por medio de la pérdida de empleos y la autoridad del gobierno de intervención en libertades personales [41].

Otro grupo pequeño, formado por un conjunto de 12 ciudadanos australianos, fue expuesto a vasta información entregada por expertos y deliberación con respecto al tema de los impuestos a bebidas azucaradas. De manera unánime, hubo apoyo a una medida fiscal en torno a las bebidas azucaradas en conjunto con medidas de etiquetado nutricional, para enfrentar la problemática de la obesidad, sobre todo infantil [42].

• Proceso político, diseño, implementación y otras consideraciones: una investigación cualitativa realizada en el año 2015 tuvo por fin explorar el contexto político; además de los objetivos, argumentos y tácticas empleados por partidarios y adversarios ante el alza de impuestos de 5% a bebidas azucaradas implementada en Chile como parte de la Reforma Tributaria de la Presidenta Bachelet. Dentro de la estrategia utilizada por los partidarios de la medida, destaca la exposición de cifras de obesidad nacional en conjunto con evidencia internacional sobre las medidas fiscales para afrontar este problema y la diseminación de la información por medio de voces validadas de la sociedad civil y de la academia. Se planteó por parte de sus detractores la inexistencia de estudios de efectividad locales que respaldaran la política como un importante argumento en contra de la medida. Además, se identifica la necesidad de un abordaje global para enfrentar el problema de la obesidad en todas sus aristas, recurriendo a alianzas consolidadas y estratégicas entre distintos actores con el fin de generar a futuro eventuales políticas fiscales de mayor solidez [44].

Por otro lado, destaca un trabajo realizado por Chriqui y colaboradores en 2013, que da cuenta de los principales aspectos que se deben tener en consideración ante el diseño e implementación de una política fiscal a bebidas azucaradas:

i) Tipo de impuesto, su aplicación y modo de recaudación.

ii) Tipos de refrescos gravados.

iii) Tasa aplicada.

Como corolario, sugiere que los países con intenciones de implementar estos tipos de impuestos deben apuntar a diseñar una política que genere el mayor aumento de precio posible. Además propone el incentivar el consumo de otras alternativas saludables, por ejemplo, agua embotellada en caso de las bebidas azucaradas [46].

Complementario al punto anterior, Jou y Techakehakij realizan un análisis de las consideraciones locales ante una política fiscal de esta naturaleza. En su análisis concluye acerca de tres aspectos clave a tener en cuenta para la implementación exitosa: la prevalencia local de obesidad; las cifras de consumo local de bebidas azucaradas; y la existencia (o no) de un impuesto similar vigente. Los autores destacan en sus conclusiones la importancia de conocer en profundidad la realidad local, en términos de patrones de consumo, sustitución y apoyo político a este tipo de medidas [45].

Min realiza un análisis del contexto e implicancias que tuvo el proyecto de restricción a la venta de bebidas azucaradas en la ciudad de Nueva York. Cabe destacar que, previo a su puesta en marcha, esta medida de restricción se “aborta” por orden judicial, por considerarse inconstitucional (ante el atropello a libertades personales) y carente de sustento teórico. Con respecto a las dificultades que pudiesen surgir en la implementación de un impuesto a bebidas azucaradas, Min identifica al lobby realizado por la industria asociado a la eventual impopularidad de un impuesto por altas tasas de consumo general. Además, al realizar una comparación con medidas fiscales a otros productos como tabaco, existe una menor conciencia de los efectos nocivos y la potencial adicción que las bebidas azucaradas pueden causar, entre otros. Esto limitaría la aceptación de una medida de esta naturaleza [62].

Un estudio de modelamiento realizado por Briggs y colaboradores [63], investiga las potenciales respuestas de la industria manufacturera de bebidas azucaradas en el Reino Unido, ante un impuesto a estos productos. Se analizan tres alternativas: reformulación del producto con disminución del contenido de azúcar, aumento de su precio y cambio en las ofertas del mercado con introducción de productos símiles con menor azúcar. Ante estos tres escenarios, se modeló el impacto en salud, evidenciando, una respuesta positiva a través de una disminución de la prevalencia de obesidad en 0,6% aproximadamente, independiente de la respuesta adoptada por la industria.

• Consideraciones de equidad: un impuesto regresivo es aquel que impacta en mayor medida a la población más pobre, quienes destinan para su pago una proporción mayor de su renta que aquellos con ingresos altos. Debido a que los hogares de menores ingresos destinan una proporción más grande de su presupuesto en alimentación [64], se ha planteado la eventual regresividad de un impuesto de esta naturaleza [65]. Sin embargo, la evidencia demuestra que un impuesto a las bebidas azucaradas tendría mayor impacto en la salud de grupos socioeconómicos más bajos, disminuyendo en mayor medida el consumo debido a que su demanda es más elástica a los precios [8],[9],[10],[12],[14],[15],[16]. Asimismo, debe considerarse que las cifras de obesidad en Chile son mayores en grupos socioeconómicos bajos, por lo que potencialmente este grupo es el que más beneficios sanitarios obtendría. Finalmente, considerando que el gasto de la recaudación fiscal es progresivo, es probable que los efectos netos de la medida sean neutros o progresivos.

• Potenciales efectos negativos:

Empleos: con el fin de medir un potencial impacto en el empleo de la población, Powell y colaboradores realizaron una simulación ante una tasa de 20% en bebidas azucaradas en los estados de Illinois y California para el año 2012. Con ella, se demostró un aumento en las cifras de empleo en ambos estados de 0,06% y 0,03% respectivamente. Si bien se detecta una eventual disminución de empleabilidad en la industria de los bebestibles, esta baja queda subsanada ante la creación de otros puestos de trabajo en sectores gubernamentales y otras industrias. Los autores hacen mención a que es importante tomar en consideración el que, aún en ausencia de impuestos a bebidas azucaradas, datos estadounidenses afirman que la empleabilidad en esta industria ha disminuido 30% en el período 1992-2007 [47].

Sustitución: utilizando datos primarios provenientes de compra en población norteamericana, se estimó el efecto de un impuesto del 20% a bebidas azucaradas en peso corporal, asociado a sustituciones en la compra de otros bebestibles y alimentos. Los resultados del estudio reportan una disminución global en la compra diaria de 24,3 kilocalorías diarias por persona, lo cual se traduce en una baja de peso de 0,7 kilógramos en el primer año y 1,3 kilógramos a largo plazo. Ante este impuesto, aumentaría la venta de jugos frutales, aportando 2,5 kilocalorías adicionales a la compra diaria. No se encontró evidencia de sustitución a otros alimentos azucarados (galletas y dulces) y se reporta además una disminución de compra de otros productos complementarios, como snacks salados [48].

Conclusiones

La búsqueda bibliográfica arroja información valiosa a considerar en el proceso de información y toma de decisión de una política fiscal de este tipo. Los hallazgos con respecto a la demanda del producto gravado, en este caso las bebidas azucaradas, son consistentes con los reportes previos de la literatura, con elasticidades persistentemente negativas, lo que demuestra que el consumo de este tipo de producto es efectivamente sensible al precio de venta, tanto en estudios de modelamiento como en experiencias locales, concordante a la racionalidad económica que sustenta estas medidas. Con respecto a los precios después del impuesto, un estudio en población mexicana reporta el traspaso del 100% del impuesto al consumidor final, lo que es consistente con la evidencia al respecto del tema [4]. En el caso de la experiencia en Berkeley, tal como fue descrito previamente, las consideraciones geográficas de la localidad pueden explicar los hallazgos del estudio, con cifras de traspaso a los consumidores bastante menores.

En lo referente a los estudios asociados al consumo de la población, destaca un estudio pseudoexperimental aplicado por Colchero y colaboradores en población mexicana [16]. En él se evidencia una disminución importante del consumo ante un impuesto de un peso mexicano por litro (alza aproximada de un 10% del precio), alcanzando a 17% en grupos de nivel socioeconómico bajo. Cabe destacar la importancia de analizar la experiencia mexicana para aprender lecciones que puedan ser aplicables en Chile. Ambos países presentan similares cifras de sobrepeso y obesidad, además de alto consumo de bebidas azucaradas, por lo que será importante valorar las lecciones que surjan desde México ante una eventual aplicación de un impuesto en Chile.

Los estudios que evaluaron impacto en peso corporal correspondieron en su gran mayoría a estudios de modelamiento. Ello, debido a las dificultades existentes para realizar estudios de seguimiento a largo plazo que permitan observar cambios en los resultados en salud luego de la implementación de estas medidas. Ante las distintas alternativas fiscales, destaca una mayor efectividad en disminución de peso corporal de los impuestos volumétricos versus los impuestos ad valorem. El impuesto volumétrico tendría la capacidad de disminuir el consumo en toda la población, pero especialmente en altos consumidores, quienes tendrían mayor prevalencia o riesgo de obesidad [18].

Independiente del tipo de impuesto aplicado, la evidencia demuestra que un aumento de precio del producto gravado en 20% es lo óptimo para generar impacto en salud, aunque aquellos aumentos de precio entre 10 y 20% también tendrían efectos positivos. La reforma tributaria en Chile, vigente desde el año 2014, generó un aumento de precio en bebidas azucaradas de 5%. Si bien esta medida se planteó con fines recaudatorios más que sanitarios, los hallazgos de esta investigación, definen que aumentos de precio menores a un 10% tienen menos probabilidades de generar impactos positivos en resultados sanitarios.

Ante un impuesto a bebidas azucaradas, surgen múltiples consideraciones en torno a la implementación. La opinión de la población general ante estos impuestos es diversa, aunque aparentemente en su mayoría es positiva por parte de población normopeso, de niveles socioeconómicos altos y cuando se esgrime el argumento de los altos índices de obesidad infantil para su aplicación. La información y educación poblacional al respecto es un factor clave a considerar en cualquier proceso de implementación de este tipo de medidas. Es necesario hacer público el problema de la obesidad nacional, los altos índices de consumos de bebidas azucaradas y la naturaleza de una política fiscal para complementar el abordaje de esta problemática en el país. La opinión de actores involucrados en procesos de decisión de políticas sanitarias, particularmente la industria, es más crítica que la de la población general, aduciendo principalmente a efectos negativos sobre la economía de una medida fiscal de este tipo, en relación a la potencial disminución de puestos laborales. Las aprehensiones asociadas a la empleabilidad, son recurrentes, pese a que la evidencia al respecto es marginal, por lo que será importante abordarlas en el proceso de información ante la implementación de una política de esta naturaleza.

Con respecto a la investigación cualitativa que estudió el contexto político vigente en Chile [44] ante el alza de impuestos a bebidas azucaradas incluida en la última reforma tributaria, es posible destacar positivamente la inclusión del tema de la obesidad y bebidas azucaradas en la agenda legislativa. Si bien, como se mencionó anteriormente, el fin de esta reforma fue principalmente recaudatorio y el aumento de la tasa fue discreto, la modificación tributaria implementada permitió poner este tema en la agenda pública, generando opiniones tanto de partidarios como adversarios de la medida. La investigación reportó dificultades importantes en el proceso de toma de decisión, principalmente la ausencia de evidencia nacional en relación al tema. Estos aspectos deberán tomarse en consideración, en caso de proponer nuevos aumentos al impuesto vigente.

Los hallazgos de la búsqueda bibliográfica dan cuenta de que las políticas fiscales a bebidas azucaradas para enfrentar las altas cifras de obesidad son estrategias vigentes que han congregado importante atención a nivel mundial, con evidencia positiva en torno a su efectividad. Chile presenta cifras importantes de obesidad, asociadas a un alto patrón de consumo de bebidas azucaradas. Esto lo posicionan como un país que potencialmente podría verse beneficiado ante la implementación de una medida de esta naturaleza. Si bien la evidencia al respecto es amplia, aún faltan más estudios de alta calidad, que permitan proyectar el impacto de la aplicación de un impuesto a bebidas azucaradas en Chile con fines sanitarios.

Los positivos resultados de los estudios de simulación de efectos a mediano y largo plazo entregan información sugerente de los potenciales efectos de una medida de este tipo en la población chilena. A través de la búsqueda realizada, se comprueba que se trata de un tema de alto interés en países que presentan altas prevalencias de obesidad. Además, debe destacarse que la evidencia que respalda su aplicación es creciente. Si bien se reconoce la necesidad de incrementar la evidencia disponible en población chilena, los hallazgos de la literatura internacional disponibles permiten avanzar en la discusión de posibles cursos de acción de manera informada.

Las medidas fiscales a alimentos para enfrentar los problemas de obesidad de la población son alternativas viables y promisorias. Estas deben considerarse como parte de una estrategia integral del enfrentamiento a un problema complejo y multifactorial como la obesidad. Ninguna estrategia, por sí sola, puede dar respuesta efectiva al problema sanitario asociado a las altas cifras de obesidad. A lo largo de las últimas décadas, Chile ha presentado múltiples medidas para enfrentar las cifras de obesidad nacionales. Sin embargo, la prevalencia aún mantiene su tendencia al alza. En este sentido, sería interesante estudiar y planificar la aplicación de una política fiscal a bebidas azucaradas en Chile con una perspectiva sanitaria, con el fin de ampliar los frentes de lucha contra la obesidad nacional de manera exitosa.

Anexos

Metodología

En marzo de 2017 se realizó una búsqueda bibliográfica en MEDLINE/PubMed, Epistemonikos, Health Systems Evidence, Cochrane y Scholar Google, con el fin de identificar las publicaciones pertinentes a esta investigación. Se utilizaron los términos Sugar sweetened beverages, Soda, Obesity y Tax. La búsqueda se limitó desde mayo de 2011 a marzo de 2017, dando como resultado 123 publicaciones de diversos tipos.

Del total de publicaciones, se incluyeron estudios que evaluaran intervenciones de impuestos a bebidas azucaradas en población general de los siguientes tipos: revisiones sistemáticas, estudios aleatorizados controlados, estudios de modelamiento o simulación, pseudoexperimentales, observacionales y cualitativos. Se evaluaron estudios que midieran resultados asociados a los efectos sobre la demanda de la población, precio del producto gravado, su consumo e impacto en salud, específicamente en torno al peso corporal. Además, se incluyeron estudios que dieran cuenta de opiniones de actores involucrados y otros aspectos asociados al proceso político, diseño e implementación de la medida.

Sobre los estudios de modelamiento y con el fin de focalizar la búsqueda, sólo se consideraron aquellos estudios que dentro de sus resultados de interés presentarán una medida de impacto de la intervención sobre la demanda de bebidas azucaradas y sobre peso corporal o índice de masa corporal de la población estudiada. Se excluyeron estudios enfocados en otro tipo de resultados en salud.

Con respecto a la bibliografía de temas de procesos políticos, diseño e implementación, se tomó también en cuenta la evidencia bibliográfica que diera cuenta de opiniones de expertos y las experiencias de implementación local. Además, se complementó con búsquedas en manuales de citas y se realizó una indagación dirigida en la literatura gris referida a experiencia nacional sobre políticas fiscales a bebidas azucaradas.

Las consideraciones anteriores determinaron un total de 54 publicaciones para su análisis. Para aquellos estudios en que fue posible debido a su metodología, se realizó una evaluación de la calidad de la evidencia utilizando las guías GRADE [66].

Notas

Declaración de conflictos de intereses

Los autores declaran no tener conflictos de intereses y declaran no haber recibido financiamiento para la realización del reporte; no tener relaciones financieras con organizaciones que podrían tener intereses en el artículo publicado, en los últimos tres años; y no tener otras relaciones o actividades que podrían influir sobre el artículo publicado.

Financiamiento

Los autores declaran que no hubo fuentes de financiación externas.